Understanding boAt’s Business Model and IPO Strategy

“You’ve plugged into Nirvana!”

The moment you hear it, you know it’s boAt.

OK, you might not know the tune, but most likely you know the brand— and its co-founder, Aman Gupta. With his unforgettable presence as an investor on “Shark Tank India”, he has become the face of boAt’s innovative and entrepreneurial spirit.

boAt devices are a go-to for many of us, right? With over 30 lakh loyal customers, it has created a vibrant community of “boAtheads”.

As per the latest updates, this widely popular company might go public in the coming year (2025).

Back in 2022, boAt filed its DRHP but withdrew it due to unfavourable market conditions (reason stated by some sources). If you're not familiar with the details, no worries—scroll down to catch up on the IPO information.

Along with it, the article covers boAt’s fundamentals, product range, financials and peer comparison, giving you a complete picture of the brand. Let's get started!

Table of Contents:

a. IPO Details

e. Conclusion

boAt IPO Details

Founded in 2014 by Aman Gupta and Sameer Mehta, the company quickly rose to prominence by offering stylish, high-quality products at affordable prices.

Here’s what the IPO’s DRHP looked like back then:

|

If you look at the OFS value in its DRHP, it shows the stakeholders selling their respective shares as:

-

Sameer Mehta (Promoter): up to ₹150 crore

-

Aman Gupta (Promoter): up to ₹150 crore

-

South Lake Investment Ltd. (Investor): up to ₹800 crore

Even though its IPO plan was postponed, the company had already privately raised funds in the same year, 2022.

A total of ₹500 crore was raised through convertible preferred stock notes from two of its investors– Warburg Pincus (existing) and Malabar Investments (new). boAt had put a minimum valuation cap of ~₹9,739.2 crore ($1.2 billion) for this fund-raising round.

If the news is true and boAt is gearing up for its IPO in FY25, then the expected details are as follows:

- Plans to raise: ₹2,535-₹4,225 crore

- Expected valuation: Over ₹12,675 crore

The above figures (taking the FY24 currency exchange rate as ₹84.5) may vary as the IPO approaches.

And the bankers– ICICI Securities (lead banker), Goldman Sachs, and Nomura are already finalised for the IPO.

Being an investor, it’ll always be your decision whether to invest in an IPO or not. But I can surely recommend you stick to your habit of understanding the company’s fundamentals before investing (assuming it has already become a habit till now).

So, let’s start with understanding boAt as a company and its business structure.

boAt’s Business Model

boAt is the leading player in the digital-first consumer technology space, offering products such as headphones, earphones, speakers, soundbars, wearables, and related accessories.

Audio and wearable products already existed in the market. But boAt’s pocket-friendly prices, unique designs and features helped the brand gain popularity, especially among India’s young, tech-savvy crowd.

Moreover, boAt’s product lineup comes under these 3 categories:

- Audio: These products are in high demand, making this category contribute the majority of its revenue (79.3% out of the sale of products).

- Wearables: Its entry into the smartwatches and smart rings category has created a growing revenue stream (17.3% out of the sale of products).

- Others: Products like cables, chargers, grooming kits, and gaming gear add a smaller yet potentially increasing revenue (3.4% out of the sale of products) it.

boAt's revenue figures below show its market standing in the past 3 years:

The company's revenue model is simple: it designs, sources, and sells products to consumers through multiple channels. boAt’s revenue figures below show its market standing in the past 3 years:

|

Revenue Category |

FY22 |

FY23 |

FY24 |

Trend Analysis |

|

Sale of Products: |

2,870.76 |

3,243.29 |

3,101.07 |

13.4% increase in FY23; 4.8% drop in FY24 |

|

2,276.02 |

2,350.83 |

2,459.20 |

Steady growth |

|

515.51 |

783.17 |

536.50 |

51.8% growth in FY23; decline in FY24 |

|

79.24 |

109.28 |

105.37 |

Growth in FY23; slight decline in FY24 |

|

Other Operating Income |

2.14 |

15.12 |

2.71 |

Significant hikes in FY23; decline in FY24 |

|

Total Revenue (Sale of Products + Other Operating Income) |

2,872.90 |

3,258.40 |

3,103.78 |

13.4% increase in FY23; 4.7% drop in FY24 |

As of the second quarter of 2024, boAt's market share is 26.7%.

Wondering how it currently holds this position in the electronics market?

Well, it's largely known through its:

- Prices

- Design

- Brand Ambassadors

- Sales Channels

Want to know what makes boAt a success? Find out in our article here in detail!

Its audio segment grew, despite the downfall in wearables sales as per the table above.

The decline in smartwatch shipments in the September quarter hints that— consumers aren’t upgrading their smartwatches as quickly as the industry has expected, leading to rising inventory levels. Even boAt's management has indicated that it is aiming to grow its wearables segment as a secondary focus.

However, for a better (or should I say in-depth) understanding of how these segments contribute to boAt’s overall performance, have a look into its finances in the next scroll.

boAt's Financials

The brand saw impressive revenue growth from FY22 to FY23, indicating a rising demand for its products. This success is likely driven by its strong brand appeal, wallet-friendly pricing, and expanding product portfolio, especially in the wearables segment.

Despite all this, its revenues took a slight fall in FY24, possibly due to rising competition in the consumer electronics space, shifting consumer preferences, or supply chain challenges.

Key Financial Data (all figures in ₹ crore unless otherwise stated)

|

Particulars |

FY 2021-2022 |

FY 2022-2023 |

FY 2023-2024 |

|

Revenue from Operations |

28,72.901 |

32,58.404 |

31,03.778 |

|

Profit/(Loss) for the year |

1,09.042 |

(1,01.122) |

(53.593) |

|

Total Debt |

9,34.697 |

12,54.769 |

8,86.776 |

|

Total Equity |

6,10.150 |

5,12.978 |

4,71.547 |

|

Debt/Equity Ratio |

1.51 |

2.41 |

1.82 |

|

Cash and Cash Equivalents (C&CE) |

30.222 |

1,39.227 |

53.264 |

Meanwhile, FY24 also brought losses for the company, but they were notably reduced, reflecting improved cost management and operational efficiency.

The Debt/Equity Ratio jumped in FY23, which may be due to higher reliance on debt for expansion and operations, but it increased financial risk. In FY24, the ratio decreased, probably due to better management through debt repayments, equity infusions, or improved profitability.

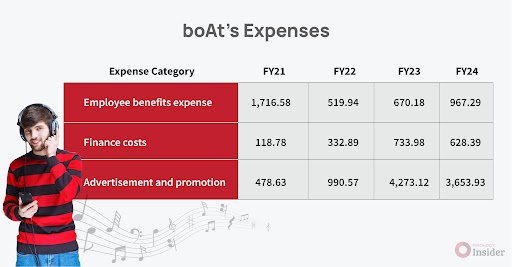

The table above shows that boAt moved from profit in FY22 to significant losses in FY23, possibly due to increased expenses for raw materials, marketing, employees, and finance from debts amid high interest rates.

It also depends on contract manufacturers for its production. In FY23, boAt formed a joint venture with Dixon Technologies (India) Ltd. to manufacture:

- Bluetooth audio devices (excluding Bluetooth speakers and home audio)

- Other mutually agreed electronic products

In fact, Dixon Technologies produces around 60-65% of boAt’s overall product volume.

To further reduce raw material costs, BoAt has partnered with over 13 contract manufacturers in India, in addition to Dixon Technologies. Notable collaborations include Bharat FIH, Foxconn, VVDN Technologies, and ILJIN Electronics.

Talking about Foxconn, did you know it's taking "Make in India" to the next level by bringing iPhone manufacturing here? Get the full story here!

And boAt's expanding products strategy extends beyond organic growth. The company has made strategic acquisitions to diversify its product range and enhance its market presence.

- TAGG: Acquired in June 2021, this brand offers wearables, which is expected to boost boAt's expansion in this category.

- RedGear: This brand, acquired in 2020, offers gaming accessories such as wired and wireless headsets, mics, and keyboards, further broadening boAt's product portfolio.

Ok, now, one question for you: 👇

Do you know which boAt’s competitor initially started as a smartphone covers company?

boAt’s Peer Comparison

The answer is Noise!

Even when I think of buying earbuds or a smartwatch, 2 brand names instantly pop up in my head– Fire-bolt and Noise.

Obviously, this is for me. You might look for some other brands for the gadgets. But it’s not wrong to say that these two names are giving a tough fight to boAt.

-

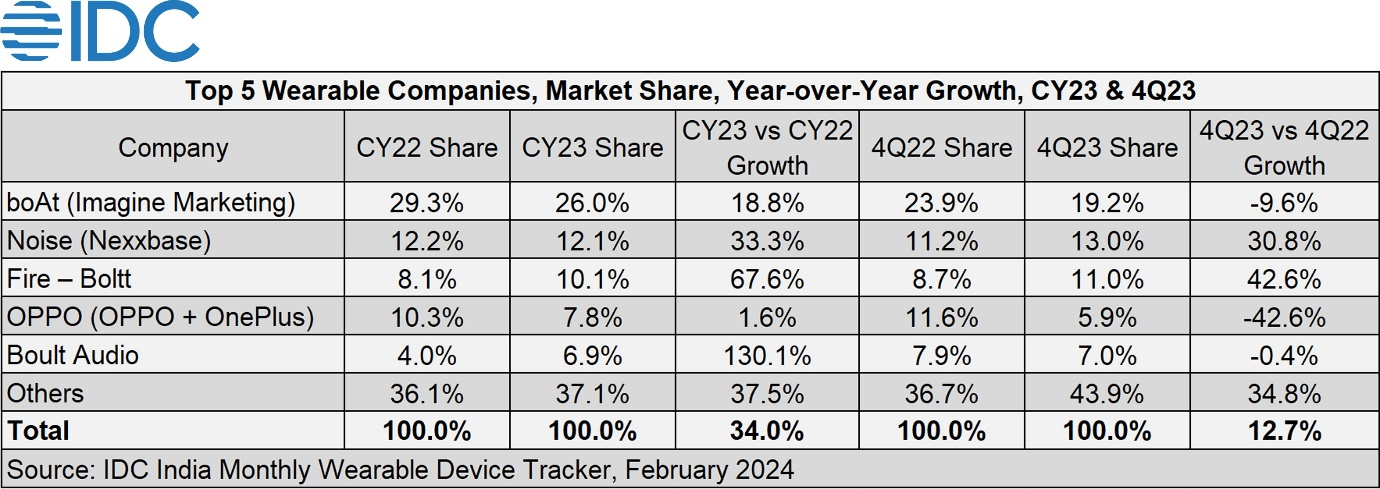

Smartwatches and wearables are taking a hit, with Fire-Boltt (6.8%) and Noise (27.4%) aggressively stealing market share through better growth strategies and unique products lineups.

-

Even Titan (12.60%) is jumping into the game, bringing its traditional brand value to the rising tech-driven wearable segment.

-

Despite maintaining category leadership, boAt’s market share has dropped by 16.1%, indicating pressure from competitors like Noise.

|

Company |

FY23 Revenue (₹ crore) |

FY23 Profit/Loss (₹ crore) |

|

Fire-Boltt |

47.28 |

21.01 (Profit) |

|

Noise |

1,426.50 |

0.90 (Profit) |

|

BoAt |

3,258.40 |

-101.05 (Loss) |

Here are the financial figures of multiple brands who are trying to pull the market share towards them from boAt:

The Bottom Line

From mid-range to premium ones, boAt has sold ~5 crore products so far, which has helped it become the market leader in electronics and smart wear.

Although it’s a big name in the market at present, its losses, other financials, and pressure from competitors cannot be ignored.

So, if the brand is planning to bring its IPO, then all eyes will be on its performance to see whether it can reach up to its high expectations or not.

Do you think boAt’s IPO will be a hit?

I’d love to hear your predictions in the comments below.

*Disclaimer: The stocks, companies, and policies discussed above aren't recommendations from Finology Insider and shall not be construed as a replacement for professional advice. Consult a professional or conduct the necessary research before making investment decisions.

How was this article?

Like, comment or share.

4

Liked this article?

You’ll love our

Premium offerings

even more.

Get access to premium content, courses, and expert tools built for investors like you.

Subscribe NowYou get all of these in one, with ONE.